Our last piece, Quick Thoughts, generated one of the highest open rates of any Economic Update we’ve sent, so we’ll take that as a clue and stick with the format.

Before we get started, we would like to make a short comment on Robin Williams life and death. While he, quite sadly, was not the only one who ended his life last week, his death does serve as a powerful reminder that everything may not always be as it seems. Madison Avenue doesn’t represent who we truly are, but what the world so vainly wants us to be. Slow down, love more deeply, and take a hike, I tell myself. Don’t let the stock market become your golden calf. (View a printable version of this Economic Update: Quick Thoughts 2).

How was my vacation? Exactly what I needed. And to my family’s pleasure, I didn’t just stare at the trunk of a coconut tree, I also swam with the stingrays. Now, for the boring stuff…

- Correction Chatter. We’ve noticed a considerable spike in anxiety levels over a looming correction, both in the media and among the folks we talk to on a day to day basis. With the market pulling back a tad from recent all-time highs, perhaps some anxiety is to be expected. But let’s get real. We can’t recall a single correction where so many got it so right!

- Earnings. While a handful of companies still have to report their second quarter results, the majority that have already done so have been a stellar lot. According to work from Francois Trahan at Cornerstone Macro, the number of CEO’s raising their future earnings guidance reached a three year high in recent weeks. The earnings results for the Broadleaf Growth Equity Portfolio have also been quite strong, with the average holding generating 38% earnings growth on year over year revenue gains of 19%. According to our work, over the long run, earnings have the highest correlation to stock market returns, not Fed policy moves.

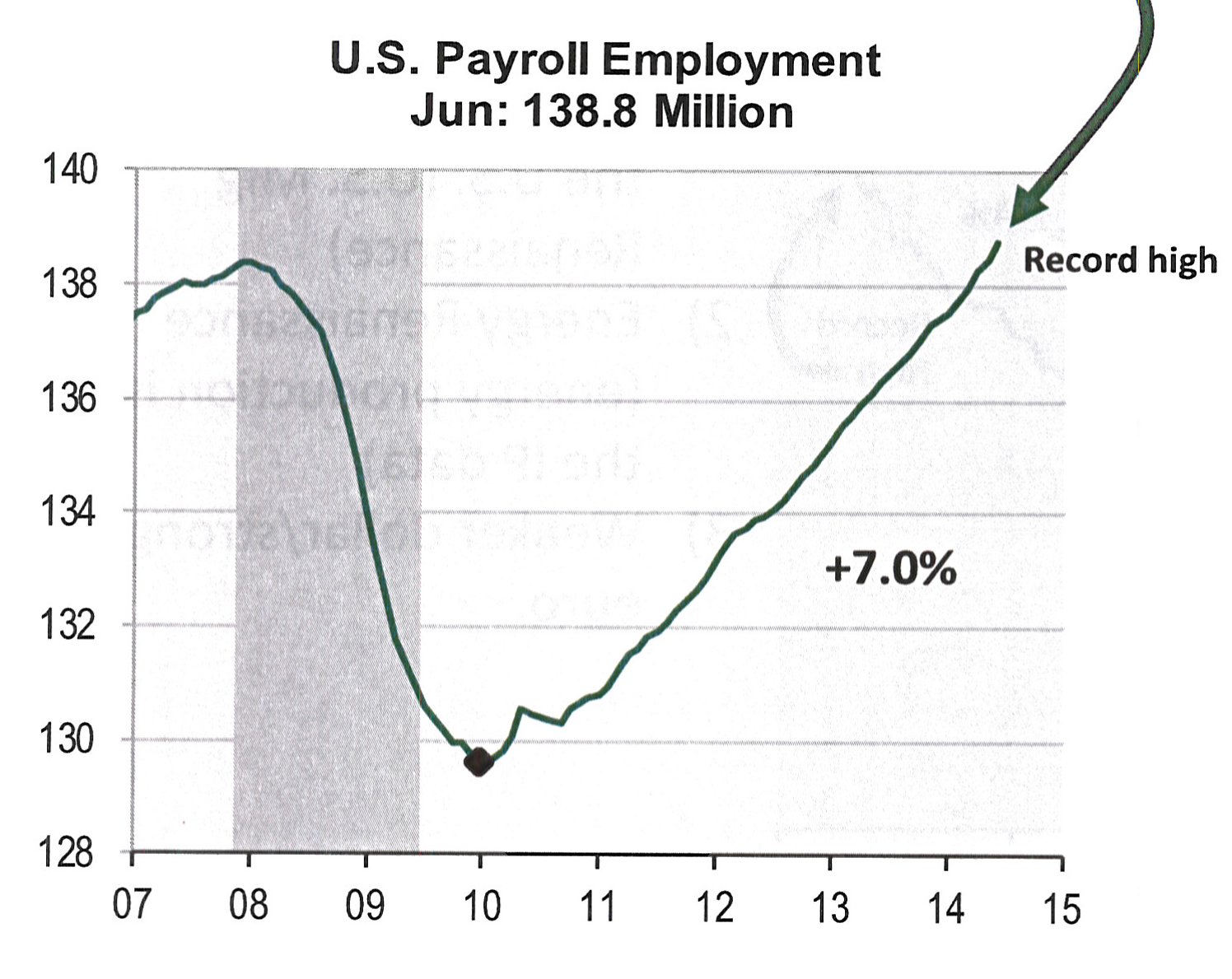

- Employment. U.S. Employment hit record highs in June, surging to 138.8 million workers. In addition, weekly unemployment claims enjoyed a downside breakout below 300,000, levels more consistent with a stable economy. While no one should get carried away with any given datapoint, the long term trend of improving employment is unmistakable. (Chart: Cornerstone Macro)

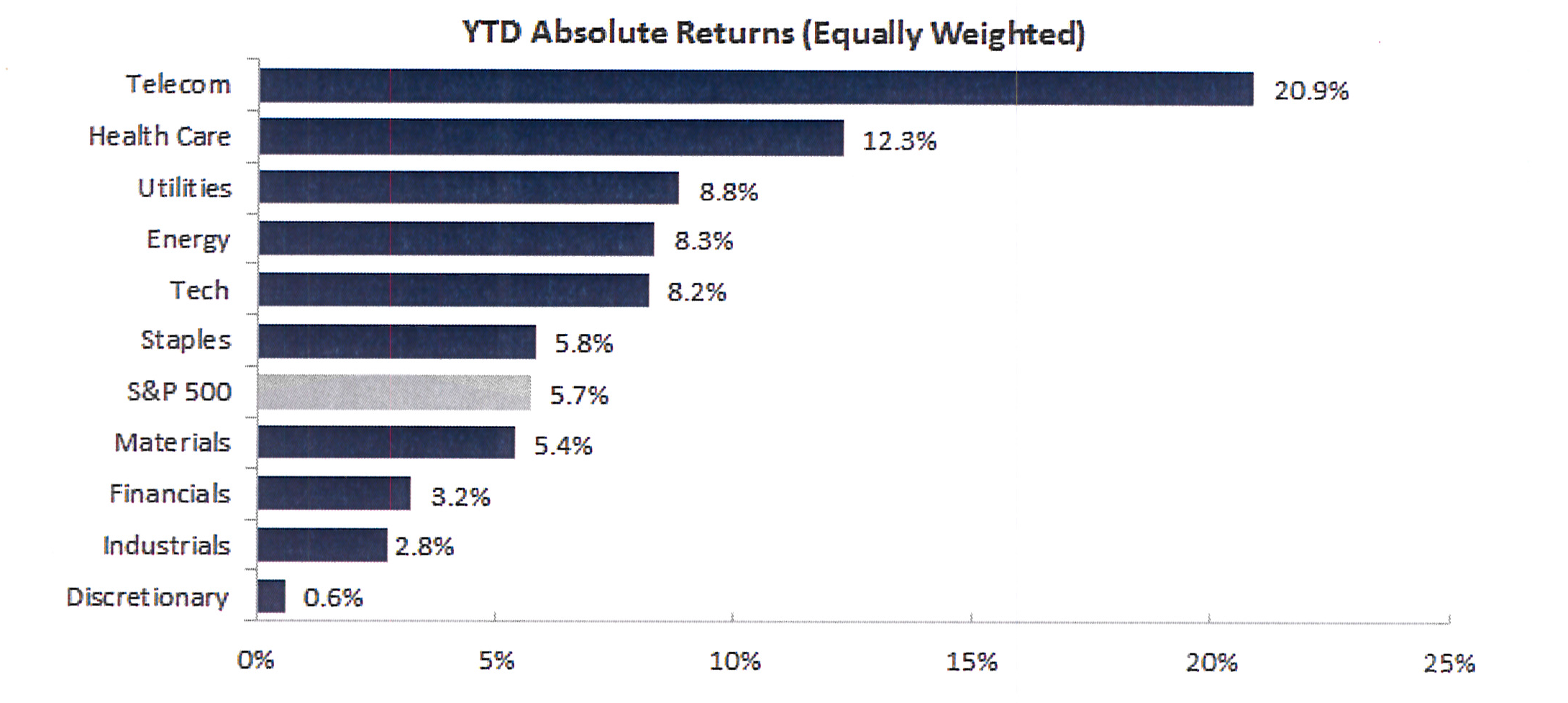

- Market Internals. Historically, the industrial and consumer discretionary sectors have had the highest correlation with S&P 500 performance returns. But this year, the two areas are the worst performing of the ten economic sectors in a reasonably strong year to date performance environment. What has worked? Telecom, health care, and utility stocks top the list, areas that are a focus of dividend investors and perhaps the more bearishly inclined. If the economy is getting better, and we believe it is, the composition of market returns should look different in the months ahead. (Chart: ISI Group)

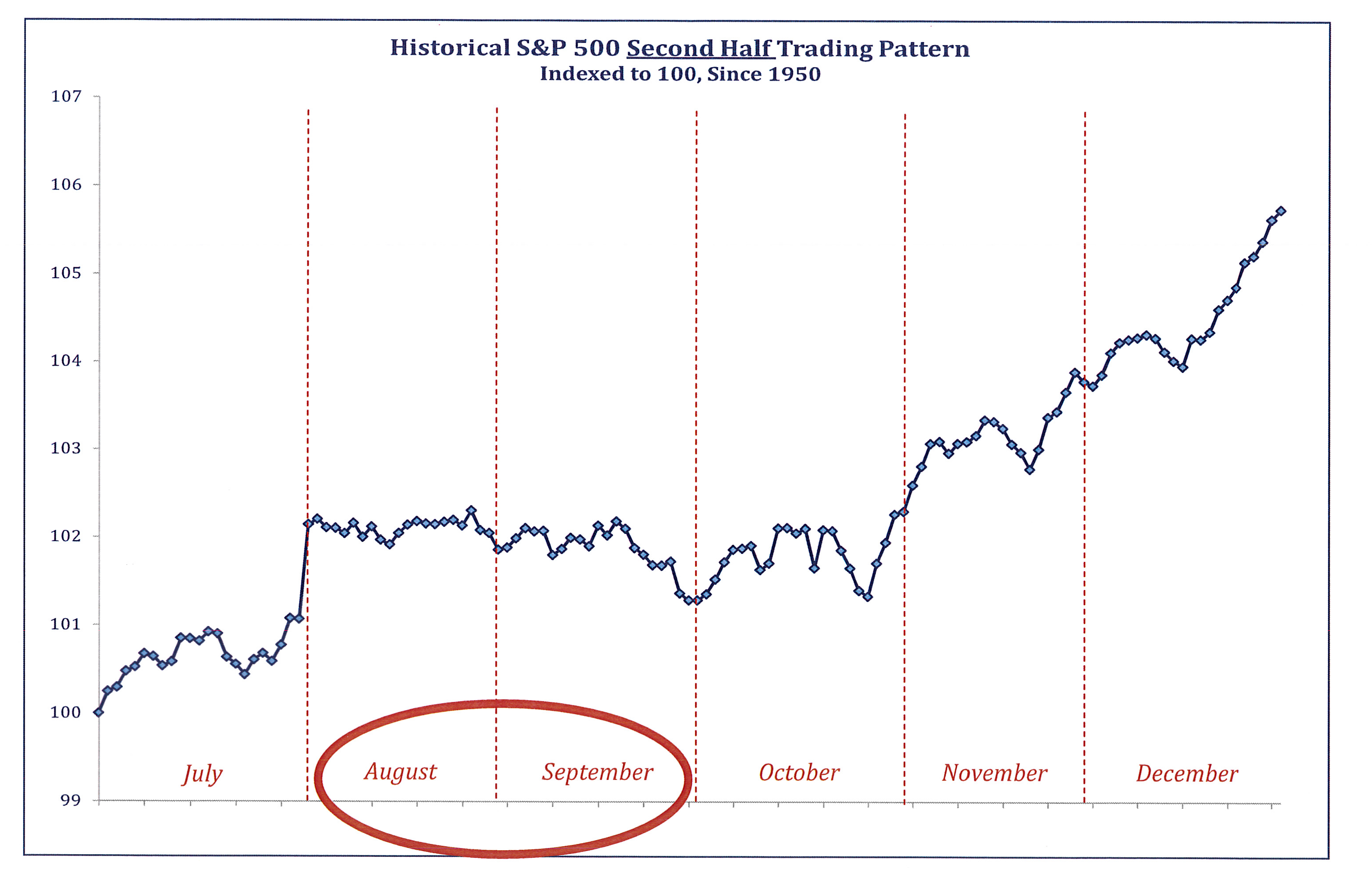

- Market Seasonality. On a related note, while we would never choose to invest based on seasonal market trends, our twenty-five years of experience in the business suggests that the second half of the year and, in particular, the last quarter, is often very kind to investors. Longer term data from 1950 on also supports this view. (Chart: Strategas Research Partners)

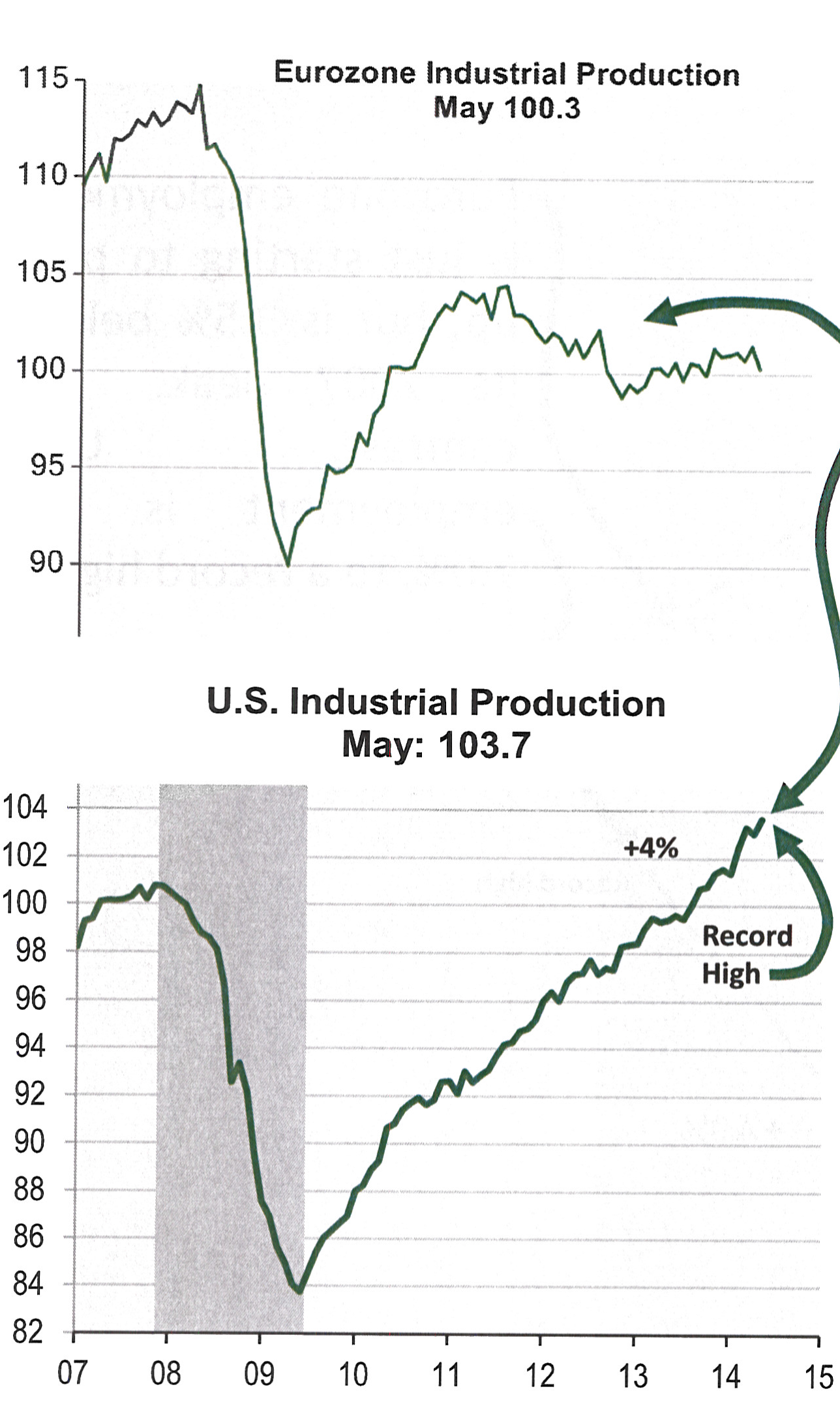

- The United States vs Everyone Else. In contrast to the United States economy, European and Asian weakness remain. Similar to the earnings and employment statistics, U.S. Industrial Production reached record highs in recent months, while similar figures in the Eurozone have flatlined for the past three years, remaining 15% below prior highs. A strong domestic economy and overseas weakness is consistent with what we’ve generally heard from second quarter earnings calls, including Cisco Systems’ last night. (Chart: Cornerstone Macro)

- The Fed. While the Fed’s influence on the markets is typically overshadowed by earnings results for a few weeks each quarter, investors seem to be more comfortable with the idea that the Fed won’t raise rates if the economy isn’t self-sustaining. Independent of the Fed, we believe long term, market based interest rates could remain far lower than many expect, as a function of persistent weakness in overseas economies, the safety trade in US Treasuries, and the fact that other large foreign central banks like China remain tied to the US Dollar. At times, we’ve wondered aloud if a risk-free security should have any return at all!

- Ecommerce. Retail has been one of the weaker areas of the market during earnings season, contributing to the poor relative returns of the consumer discretionary sector. I tend to believe that the poor economy in the first quarter coupled with a decent snapback in the second, caught many apparel retailers in particular with the wrong types of inventory, resulting in a far more promotional environment. At the same time, innovators like Under Armour and Chipotle didn’t miss a beat, making the weather sound like an excuse. According to Channel Advisor data, Amazon achieved July same store sales growth of 40.4% y/y, which clearly makes WalMart’s flat results appear like a serious long term problem. While we can argue whether or not Amazon will ever be profitable, there is no doubt that the company is winning new customers at an accelerating pace.

- Oil and Inflation. We’re sounding a bit like a broken record here, but positive trends in domestic oil production are a gamechanger for our economy. Coupled with Wall Street’s obsession with asset efficiency and companies like Amazon, Uber, and AirBNB, inflation and thus interest rates, could stay low for far longer than anyone might expect. Slack remains.

As always, we welcome your comments and questions! Kindest Regards, Doug Doug MacKay CEO & CIO dmackay@broadleafpartners.com Bill Bill Hoover President bhoover@broadleafpartners.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}